Guidance Notes on Sections 5(1A), 5(1B), 5(5) and Schedule 11 – Business Tax Act (2009)

Table of Contents

- Introduction

- When to apply Section 5(1A): Is the company both a ‘resident company’ and a ‘covered company’?

- How to apply Section 5(1A) to income: which sub-section applies?

- How to apply Section 5(1A) to income: ss (a) to (d)

- Schedule 11 substance test

- Miscellaneous

- Appendix – Flowchart

1. Introduction

These guidance notes have been prepared by the Seychelles Revenue Commission (“SRC”) concerning the amendments to the sourcing rules introduced by the Business Tax (Amendment) Act, 2020. These notes provide guidance on the new conditions imposed for “covered companies” in respect of the Seychelles’ sourcing rules set out in Sections 5(1A), 5(1B) and 5(5) of Business Tax Act (Cap 20), including a substance test for foreign passive income in Schedule 11. “Covered companies” are those companies that meet the test set out in Paragraph 1 of Schedule 11. Where a covered company fails to meet the new conditions, including the new substance test, the foreign income derived by the company will be deemed to be Seychelles sourced income.

These guidance notes supplement those on the Seychelles sourcing rules in general which are set out in the SRC guidance notes “Income sourced in and from Seychelles”. The sourcing rules set out in Section 5(1) will continue to apply to companies that are not “covered companies”. The broad guiding principles set out in that guidance will also be helpful in considering the new conditions applying to the sourcing rules for “covered companies”. Many of the key concepts around what is, and is not, Seychelles’ sourced income apply as much to the new sourcing rules in Section 5(1A) as they do to the rest of Section 5.

The Seychelles operates a self-assessment tax regime. As with other tax provisions, it is the responsibility of a company incorporated or operating in Seychelles to determine if it has Seychelles sourced income in a tax year. These guidance notes are intended to assist in understanding when and how to apply the new provisions at Section 5(1A). Where the provisions apply, a company may need to account for tax on additional sources of income in its annual Business Tax Return (see the SRC’s “Business Tax Guide” on completing these returns). In some cases, companies may be completing a Business Tax Return for the first time.

1.1 Background on the Seychelles territorial regime

The Seychelles has historically operated a territorial tax regime, meaning that only income sourced in Seychelles was liable to tax in Seychelles. Income was considered Seychelles’ sourced income exclusively where it arose from business “activities conducted, goods situated or rights used” within the physical territory of Seychelles. This meant that income was considered non-Seychelles sourced income (i.e. “non-taxable business income”) where the income was:

- from activities conducted by a Seychelles business in an overseas jurisdiction (through a branch, office, shop or otherwise); and

- in the form or dividends, interest, royalties, rents and other “passive income” received by a Seychelles resident from a non-resident.

The changes of law applying from 16 September 2021 adopts a revised approach for covered companies, including the adoption of an economic substance test for passive income received from a non-resident.

1.2 Changes to the Seychelles territorial regime given Presidential assent on 28 December 2020

On 28 December 2020, the President of the Republic of Seychelles gave his assent to the Business Tax (Amendment) Act, 2020 which amended the Business Tax Act (Cap 20). However, the Business Tax (Amendment) Act, 2020 only came into operation on 15 September 2021, and Schedule 11 was amended by Regulation the next day.

Consequentially, Sections 5(1A), 5(1B) and 5(5) and Schedule 11 (and consequential amendments) therefore came into effect on same aforementioned dates.

1.3 Outline of these guidance notes

These guidance notes are designed to help a company’s directors or, where applicable, registered agents to understand when and how to apply the new rules.

It does this, by:

- Focusing on when a company will need to consider the application of Section 5(1A) Business Tax Act (Cap 20), and

- How it should apply its provisions to income arising to the company in the year.

In doing so, it also:

- Discusses the application of Sections 5(1B) and 5(5), and

- Considers the application of the adequate economic substance test in Schedule 11.

All legislative references in these guidance notes are to the Business Tax Act (Cap 20), unless otherwise stated.

| Does Section 5(1A) apply to the company? | Which sub-sections apply, and how, to income arising to the Company? | If applicable, how do you apply the adequate economic substance test? |

|---|---|---|

| See Part 2 | See Parts 3 and 4 | See Part 5 |

2. When to apply Section 5(1A): Is the company both a ‘resident company’ and a ‘covered company’?

As a first step, it will be necessary to determine whether Section 5(1A) applies at all. This Part provides some guidance on when to apply Section 5(1A).

Section 5(1A) only applies to:

(i) a resident company;

(ii) to which Schedule 11 applies (i.e. a “covered company”).

2.1 Is the company tax resident in Seychelles?

Any company incorporated in Seychelles is tax resident in Seychelles under Seychelles law.

However, tax treaties may apply to deem a Seychelles-incorporated company to be tax resident outside Seychelles. This will be the case where:

- the “place of effective management” of the company is located in an overseas jurisdiction with which Seychelles has a double tax treaty, and

- that overseas jurisdiction asserts taxing rights according to where the company is “managed and controlled”.

The terms of the specific tax treaty should be checked to confirm the relevant treatment. The place where a company is managed and controlled is likely to be the same as the “place of effective management”. This is likely to be where the head office is located or, where different, where the board of directors meets. This is not necessarily where the income-generating business activities and day-to-day operations take place.

2.2 Is the company a “company to which Schedule 11 applies” (i.e. a “covered company”)?

A company will only be a “covered company” if it is an enterprise that is “a member of a multinational group”.

The definition of multinational group follows that used by the Organisation for Economic Co-operation and Development (“OECD”) for Country-by-Country Reporting (“CbCR”), as set out in the Base Erosion and Profit Shifting (“BEPS”) Action 13 Final Report. The definition of multinational group is built on the standards used for determining whether the operation of two enterprises or business units should be consolidated for financial reporting purposes.

The test of membership of a “multinational group” is set out in further detail below.

For the avoidance of doubt, a company may become, or cease to be, a covered company at any point through a tax year, including when it first becomes a member or ceases to be a member of a multinational group at any point through the tax year.

2.2.1 STEP 1: Meaning of “group”

The first step is, to determine if the Seychelles company is part of a group. This test is based on a control test used for accounting. In general, the effect of this test is that two enterprises (e.g. companies) will be treated as part of the same Group where one enterprise controls the other or both enterprises are controlled by another enterprise.

2.2.2 STEP 2: Meaning of “multinational”

The next step is to determine whether this is a group which spans multiple jurisdictions. A group will be a “multinational” group where there are two or more enterprises the tax residence for which is in different jurisdictions.

This will typically require that a Seychelles company is part of a consolidating group (see below) with a parent or subsidiary that is resident in another jurisdiction outside Seychelles (further explanation of the meaning of a “consolidating group” is set out in the following subsection).

Consistent with the OECD definition used for CbCR, the definition of “multinational” also includes circumstances where an enterprise that is resident for tax purposes in one jurisdiction is subject to tax with respect to its income in another jurisdiction by reason of having a permanent establishment there.

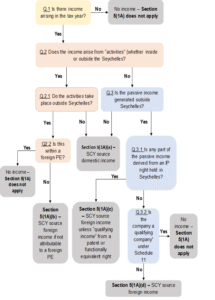

3. How to apply Section 5(1A) to income: which sub-section applies?

3.1 Q1: Is there income arising in the tax year?

3.2 Q2: Does the income arise from “activities” (whether inside or outside Seychelles)?

3.3 Q2.1: If “YES”, do the activities take place outside Seychelles?

3.4 Q2.2: If outside Seychelles, do the activities take place in a foreign permanent establishment?

3.5 Q3: If income is passive, is it generated outside the Seychelles?

3.6 Q3.1: Is any part of the passive income derived from an intellectual property right held in Seychelles?

3.7 Q3.2: Is the passive income earned by a “qualifying company”?

4. How to apply Section 5(1A) to income: ss (a) to (d)

4.1 (a) activities conducted, goods situated or rights used in Seychelles;

4.2 (b) activities conducted outside Seychelles unless attributable to business carried on through a permanent establishment of the person outside Seychelles;

4.3 (c) income derived from an intellectual property right held in Seychelles other than qualifying income from (i.) a patent, or (ii.) a right functionally equivalent to a patent;

4.4 (d) other passive income generated outside Seychelles except to the extent that the resident company is a qualifying company in accordance with Schedule 11

Passive income arising from a person or entity resident outside the Seychelles is considered Seychelles’ sourced unless the Seychelles resident recipient meets the substance requirements for this income that are set out in Schedule 11.

5. Schedule 11 substance test

5.1 Entity-based approach

Paragraphs 1 to 7 of Schedule 11 set out the substance test in respect of foreign passive income (the source of which is determined by Section 5(1A)(d)) as follows:

- Paragraph 1 states that Schedule 11 applies to an enterprise that is a member of a multinational group. The definition of multinational group, and the application of Paragraph 1 are covered at section 2.2 of this guidance.

- Paragraph 2 contains the substance test itself. A company shall be considered to be a qualifying company for the purposes of Section 5(1A)(d) if that company has adequate economic substance in the tax year. What is “adequate economic substance” for each company will depend on the particular facts of the company and the nature of business.

- Paragraph 3 provides examples of when adequate economic substance can be considered to be met. These examples are based on classifying companies into broad categories depending on the general nature of the passive assets they hold as follows:

- A pure equity holding company (defined in Paragraph 6);

- A real estate holding company (defined in Paragraph 6);

- A company “other than a pure equity holding company or real estate holding company”. This category covers companies with debt assets (i.e. loans and interest-bearing financial instruments), and/or a diversified portfolio of assets.

Companies with intellectual property assets will also need to consider Section 5(1A)(c) as discussed above at Section 4.3.

- Paragraph 4 notes that the “adequate economic substance” test may be fulfilled where the economic substance is fulfilled by third parties acting on behalf of the company, provided certain conditions are met.

It is important to note that for tax reporting purposes, the substance test in Schedule 11 Paragraph 2 is designed to be self-assessed by the company. As such, the company’s directors or representatives should make a decision as to whether the substance test is met and make a determination in good faith.

The entity-based approach in Paragraph 3 is intended to make it easier to self-assess whether the substance test is met. Under this approach, the general nature of the company rather than the nature of each passive income-producing asset can be considered.

Pure equity and real estate holding companies can be considered to have “adequate economic substance” where they meet the examples set out in:

- Paragraph 3(a), complying with applicable company filing requirements; and

- Paragraph 3(b), having adequate human resources and premises in Seychelles for holding and managing their investments;

All other companies (such as those with loans and interest-bearing financial instruments) will also need to demonstrate the substance set out in Paragraph 3(c) of Schedule 11. These “other companies” therefore need to meet a high burden of proof than pure equity and real estate holding companies in demonstrating that they satisfy the “adequate economic substance” tests.

The rest of this Part sets out further guidance on how to apply Schedule 11, including on the categorisation of companies and the particulars of the different burdens of proof.

5.1.1 Meaning of “pure equity holding company”

A pure equity holding company is a company which, as its primary function, acquires and holds shares or equitable interests in one or more other companies and performs no substantial commercial or investment activity.

The acquiring and holding of shares must be the “primary function” of the company. This means that a pure equity holding company can carry out ancillary activities, so long as these are not the main part of the company’s business.

The main income arising to a pure equity holding company is likely to be from dividends. However, this does not mean that the income of the company needs to exclusively be in the form of dividends.

The placing of dividend monies received in a foreign bank account will not preclude a company from still being regarded as a pure equity holding company, where the “primary function” of the company is still to acquire and hold shares.

A company that frequently trades in equity interests, and thereby performs trading or dealing activity in Seychelles, would have income arising from “activities conducted” in Seychelles which would be treated as Seychelles’ sourced income under Section 5(1) or 5(1A)(a).

5.1.2 Meaning of “real estate holding company”

A real estate holding company is a company which, as its primary function, acquires and holds interests in immovable property, such as land or buildings. Such interests may be in the freehold or leasehold of a property. Where it is leasehold, the ownership may be in the primary head lease or any secondary or reversionary lease interest. The main income arising to a real estate holding company should be rental income.

The same comments in relation to pure equity holding companies also applies to real estate holding companies. The acquiring and holding of interests in immovable property must be the “primary function” of the company. This means that a real estate holding company can carry out ancillary activities, so long as these are not the main part of the company’s business.

5.1.3 “Other companies” covered under Paragraph 3(c)?

All other companies that are not pure equity holding companies or real estate holding companies will need additionally to demonstrate the substance set out in Paragraph 3(c). Other companies in this context includes companies with debt assets (i.e. loans and interest-bearing financial instruments), and/or a diversified portfolio of assets.

Debt assets means those assets that produce interest income, such as loan receivables or interest-bearing financial instruments, such as:

- intra-group corporate loan notes and debentures;

- government or corporate bonds; and

- interest-bearing derivatives.

Debt assets do not include loans from banking or financing activities conducted in Seychelles. Such loans derive from activities conducted in Seychelles and should therefore any income will be treated as Seychelles’ sourced income under Section 5(1A)(a).

Companies holding a diversified portfolio of assets cannot be classed as having their “primary function” of holding shares or real estate.

5.2 Tests for “pure equity holding company” and “real estate holding company”

If a company is a “pure equity holding company” or a “real estate holding company”, it will be considered to have economic substance where it has:

- complied with all applicable filing requirements under the Companies Act 1972, or the International Business Companies Act 2016, as applicable, and

- adequate human resources and premises in the Seychelles for holding and managing its investment assets (be that equity participations or real estate).

5.2.1 Compliance with applicable filing requirements

Compliance with applicable filing requirements includes:

| In the case of a company incorporated under the Companies Act 1972: | In the case of a company incorporated under the International Business Companies Act 2016: |

|---|---|

| • Updating Register of Companies with changes to the company’s secretary, members or directors; and | • Keeping the register up-to-date for changes to the company’s members or directors; |

| • Submitting an annual return. | • Paying annual fees; and |

| • Submitting an annual return / accounting records. |

Occasionally, companies may be in technical breach of the filing requirements rule because of late filing, or because of an inadvertent error or omission in documents that are filed on time. In spite of such technical breaches, there may be circumstances where it is reasonable to consider a company still meets the test of having adequate economic substance. This is more likely to be the case where there is an inadvertent omission or error made in good faith, or where a delay is only brief and can be swiftly remedied.

However, where an omission is deliberate or a delay is ongoing this is unlikely to be considered reasonable.

The reference to filing requirements is considered to include both external requirements (such as with the ROC) and internal filing requirements (such as maintaining records at the company’s registered office).

5.2.2 Adequate human resources and premises

A company must have adequate human resources and premises in the Seychelles for holding and managing its investment assets (be that equity participations in the case of a pure equity holding company, or real estate interests in the case of a real estate holding company).

What is “adequate” in this context will depend on the facts of the company in question. As is recognised by the OECD in its substance requirements for holding companies, such companies “may not in fact require much substance in order to exercise their main activity of holding and managing equity participations”. The requirements for adequate people and premises should be assessed accordingly.

In relation to people, “adequate” means a sufficient number of suitably qualified employees. These people must have access to premises provided by the company, that enables them to carry out their functions. Alternatively, the company could have a local agent which is genuinely carrying out these active management activities on its behalf.

5.3 Tests for other types of company

In addition to complying with the requirements described above (paragraph 5.2), in the case of any other company, other than a pure equity holding company or a real estate holding company, in order to be regarded as having adequate economic substance it must also ensure that it:

(i) takes necessary strategic decisions; and

(ii) manages and bears principal risks in Seychelles; and

(iii) incurs adequate expenditure, relating to the acquisition, holding or disposal, as the case may be.

5.3.1 Meaning of “strategic decisions”

“Strategic” takes its ordinary meaning. “Strategic” can generally be taken to be “part of a long-term plan to achieve a specific purpose”. In this context, “strategic decisions” are those taken with a view to the long-term purposes of a company. Such “strategic decisions” are therefore likely to be taken by those persons authorised to make long-term decisions on behalf of the company. Who those persons are will depend on the facts, particularly the size and nature of a company’s asset portfolio.

In the case of a holding company with one asset class, the strategic-decision maker is likely to be the board of directors, since the holding of the assets in question will be central to a company’s long-term purpose and value. This would also apply to a company that holds a loan note in a subsidiary.

In such circumstances, covered companies will demonstrate strategic decision making where board meetings are held in Seychelles in relation to the key decisions affecting the assets held by the Seychelles company. Key decisions are likely to include the acquisition or disposal of an asset, or changes to the way that an asset is managed or exploited. A board meeting will need to take place in Seychelles in respect of these key decisions, as and when the decisions are made.

A company with a diverse range of assets, including highly liquid assets traded on a public marketplace (such as government bonds) might authorise employees or even third-party agents to undertake decision-making functions. This is more likely to be the case where there is a part disposal of an asset class, or where the board of directors provides a framework with the long-term strategy of the company, within which individual decisions are made.

However, the frequent trading of assets is likely to mean that income arises from “activities” in Seychelles, which would mean the income would be treated as Seychelles’ sourced under Section 5(1A)(a).

“Strategic” decision-making, can be distinguished from:

- Research/recommendations undertaken that feed into a decision taken to buy or sell an asset;

- Smaller, day-to-day decisions such as the decision to put a dividend on deposit in a bank current account.

5.3.2 Meaning of “manages and bears principal risks in Seychelles”

The principal risks in relation to the assets must be genuinely managed and born by the company holding the assets in Seychelles. The principal risks in relation to holding assets includes the potential economic loss of value in those assets. Where an asset is beneficially owned by a company in Seychelles, it is likely that the economic risk will be borne by the company in Seychelles.

The management of risks may be outsourced, provided that the outsourcing is adequately supervised and is undertaken in Seychelles (see Part 5.4 below on Outsourcing).

5.3.3 Meaning of “incurs adequate expenditure”

Adequate expenditure must be incurred in Seychelles in relation to the acquisition, holding or disposal of the assets held by the company. Where an asset is truly beneficially owned by a company in Seychelles, it is likely that an “adequate” amount of expenditure will have been incurred in acquiring it.

Zero (or minimal) expenditure may be “adequate” depending on the circumstances in which the asset was acquired: for example, if the asset was contributed to the share capital of the company by its shareholder, or if it was distributed to the company from a subsidiary.

Expenditure on the acquisition of an asset also includes ancillary expenditure, such as payments for transfer taxes, legal fees, and updates to legal registers.

An adequate amount of expenditure should be incurred in relation to the holding of the asset. For a real estate asset, this might include expenditure on maintenance or improvements to the underlying property. For an equity asset, this might include expenditure on stewardship activities (e.g. time and expenses attending shareholder meetings and reviewing performance). In either case, the expenditure should be proportionate to the level of investment.

An adequate amount of expenditure would also be expected to be incurred in relation to the disposal of the asset. This is likely to include the costs of third-party advisors, any taxes and legal fees for registration processes.

5.4 Outsourcing

The activities that a company must carry out in respect of holding and managing investments and managing risks may be outsourced to third party contractors or agents, provided certain conditions are met. These conditions are that the outsourcing company must be able to demonstrate that it has adequate supervision in the Seychelles, of the outsourced activities; and that those activities are undertaken in the Seychelles.

A company will be able to outsource activities to the extent that these conditions are fulfilled. The types of activities that can be outsourced in respect of holding and managing investments and managing risks will depend on the nature of the investment activities carried out by a company. In the case of a company holding investments for the long term, the outsourced activities may simply comprise making annual filings on behalf of the company.

Where a company actively manages its investments, and outsources some or all of that active management, then those activities must be genuinely undertaken by agents on behalf of the company. Those agents should be based in Seychelles and adequately supervised by the outsourcing company in Seychelles. Where a third party is undertaking outsourced investment management activities in Seychelles on behalf of several Seychelles clients, such outsourced activities may only be considered in relation to one client at a time.

6. Miscellaneous

6.1 Interaction of the substance test in Paragraph 2 Schedule 11

Paragraph 2 of Schedule 11 is not the only Seychelles legislation to contain an economic substance test.

Substantial activity requirements were introduced by the Securities Act (i.e. Securities (Amendment) Act, 2018) and the Mutual Fund and Hedge Fund Act (i.e. Mutual Fund and Hedge Fund (Amendment) Act, 2018. Further guidance on the substantial activity requirements is contained in the “Substantial Activity Requirements Guidelines” issued by the Financial Services Authority.

There should be no overlap between the Securities Dealers/Mutual Fund substantial activity requirements and the substance test in Schedule 11. The Securities Dealers/Mutual Fund substantial activity requirements apply to the active business conducted by licensees in those specific industries. In contrast, the Schedule 11 substance test applies only to the passive income of “covered companies”.

Appendix – Flowchart of application of sourcing rules to Seychelles entity with income of all types

Seychelles activities, foreign activities, intellectual property income and foreign passive income

Tax resident company: status

Is the company:

- A “covered company”?

No → Existing sourcing rules apply as before (Section 5(1))

- SCY source: Seychelles activity

- Non-SCY source: All foreign activity, Foreign passive income

Yes ↓

Does the company have “adequate economic substance”, Schedule 11 Para 2?

No → Non-qualifying company (S.5(1A)(d))

- SCY source: Seychelles activity, Foreign activity where no PE, All foreign passive income

- Non-SCY source: Foreign PE activity

Yes ↓

Qualifying company (S.5(1A)(d))

- SCY source: Seychelles activity, Foreign activity where no PE, IP other than “qualifying income” from R&D

- Non-SCY source: Foreign PE activity, Foreign passive income other than IP, “Qualifying income” from R&D